A credit risk is the risk of default on a debt that may arise from a borrower failing to make required payments. In the first resort, the risk is that of the lender and includes lost principal and interest, disruption to cash flows, and increased collection costs. We’ll focuse on retail banking area.

The dataset from Banque de France is composed of 10 features and 99.302 customers.

We’ll procede first to load packages and functions, and work on light data processing. At the end we’ll implement deep learning model and check output model indicators.

Configuation packages / functions

Packages: we load 5 packages for data processing, train deep learning model and indicators output

# packages

library(data.table) # for data processing

library(dummies) # for data processing

library(tensorflow) # for classification

library(keras) # for classification

library(ROCR) # to measure model performanceFunctions: functions for data processing & output model indicators

# compute lift

whatsMyLift <- function(score,cible, perc = 0.1,target){

n = ceiling(perc*length(score))

percentile = cible[order(score, decreasing = T)[1:n]]

length(percentile[percentile==target])/length(cible[cible==target])

}

# compute gini + lift

IndicatorsModels<-function(base,proba,target){

pred <- prediction(proba, FactorToBinNum(base$target,target))

perf <- performance(pred, measure = "tpr", x.measure = "fpr")

auc <- performance(pred, measure = "auc")

GiniIndex<-as.numeric(auc@y.values[[1]]*2-1)

plot(perf)

L5<-whatsMyLift(proba,base$target,perc=0.05,target)

L10<-whatsMyLift(proba,base$target,perc=0.1,target)

ResInd<-c(L5,L10,GiniIndex)

names(ResInd)<-c("Lift5","Lift10","gini")

round(ResInd*100,0)

}

# normalize vector

normalize <- function(x) {

((x - min(x)) / (max(x) - min(x)))

}

# transform vector

BinToFactor<-function(vect,NonTarget,target){

vect[vect==0]<-NonTarget

vect[vect==1]<-target

as.factor(vect)

}

# transform vector

FactorToBin<-function(vect,target){

vect<-as.character(vect)

vect[vect!=target]<-"0"

vect[vect==target]<-"1"

as.factor(vect)

}

# transform vector

FactorToBinNum<-function(vect,target){

vect<-as.character(vect)

vect[vect!=target]<-"0"

vect[vect==target]<-"1"

as.numeric(vect)

}

# split train/test

trainTestSplit <- function(df,trainPercent,seed1){

## sample size percent

samp_size <- floor(trainPercent/100 * nrow(df))

## set the seed

set.seed(seed1)

idx <- sample(seq_len(nrow(df)), size = samp_size)

idx

}

PropTable2<-function(vect){

round(prop.table(table(vect)),2)

}Data processing

Reading credit risk dataset. We use fread function from data.table package (fast read).

path<-paste(getwd(),"data",sep="/")

data<-fread(paste(path,"dataset.csv",sep="/"),sep=";",stringsAsFactors = F,colClasses = "character")

data<-data.frame(data)Processing numerical & factor features. We’ll scale et replace NA value for numerical features, and dummies the categorical features.

# select data

ListNum<-c("amount","old.work","default","time","downpayment")

ListFact<-c("type","type.work","gender","working.sector","used.car")

# numerical features processing: NA & scale

DataNum<-data[,match(ListNum,names(data))]

for (i in 1:dim(DataNum)[2]){

col<-as.numeric(DataNum[,i])

col[is.na(col)]<-median(col[!is.na(col)])

col<-normalize(col)

DataNum[,i]<-col

}

str(DataNum)

'data.frame': 99392 obs. of 5 variables:

$ amount : num 0.506 0.509 0.449 0.503 0.405 ...

$ old.work : num 0.327 0.232 0.048 0.166 0.156 ...

$ default : num 0 0 0 0 0 0 0 0 0 0 ...

$ time : num 0.514 0.667 0.667 0.5 0.167 ...

$ downpayment: num 0 0 0.434 0 0.716 ...

# factor features processing

DataFact<-data[,match(ListFact,names(data))]

for (i in 1:dim(DataFact)[2]){

col<-as.factor(DataFact[,i])

DataFact[,i]<-col

}

str(DataFact)

'data.frame': 99392 obs. of 5 variables:

$ type : Factor w/ 2 levels "PRI","PRO": 2 2 1 2 1 1 1 2 2 1 ...

$ type.work : Factor w/ 17 levels "","0","10","11",..: 6 2 6 6 4 5 4 2 4 6 ...

$ gender : Factor w/ 7 levels "","C","D","M",..: 4 2 2 4 4 4 4 2 2 2 ...

$ working.sector: Factor w/ 17 levels "AGR","ATR","BTP",..: 10 1 2 10 3 4 2 1 3 2 ...

$ used.car : Factor w/ 2 levels "VN","VO": 1 1 1 1 1 1 1 1 1 1 ...

# decompose factor dataset on dummy

DataFact<-dummy.data.frame(DataFact,sep="-")Final dataset: merge between numerical and dummies features.

# final data

data<-data.frame(DataNum,DataFact)

# numerical format

for (i in 1:dim(data)[2]){

data[,i]<-as.numeric(data[,i])

}Define the target: we just rename the target.

# define target

names(data)[match("default",names(data))]<-"target"

# target proportion

PropTable2(data$target)

vect

0 1

0.98 0.02 We see umbalanced data, we have two ways here: first we work with umbalanced data on the algorithm or we work now on the data to get balanced.

Umbalanced data

We have to deal with the umbalanced dataset: we’ll generate artifical data to get balanced.

# take umbalanced data

DataTarget<-data[data$target==1,]

d1<-dim(DataTarget)[1]

d2<-dim(data)[1]

t<-round(d2/d1,0)

res<-NULL

for (i in 1:t){

res<-rbind(res,DataTarget)

}

data<-rbind(data,res)

# mixed data

Random<-557

data_idx<-trainTestSplit(data,100,Random)

data<-data[data_idx,]

# proportion with balanced data

PropTable2(data$target)

vect

0 1

0.49 0.51 Split dataset

We just rename the target as “Default” or “NonDefault”

# named target

NonTarget<-"NonDefault"

target<-"default"

# change target to names

data$target<-BinToFactor(data$target,NonTarget,target)Split train/test set: we take 70% of train and 30% of test set

# named target

NonTarget<-"NonDefault"

target<-"default"

# change target to names

data$target<-BinToFactor(data$target,NonTarget,target)

# train and test

Random<-558

train_idx <- trainTestSplit(data,70,Random)

train <- data[train_idx, ]

test <- data[-train_idx, ]

# check target proportion on train/test dataset

r1<-PropTable2(train$target)

r2<-PropTable2(test$target)

r3<-rbind(r1,r2)

rownames(r3)<-c("train","test")

print(r3)

default NonDefault

train 0.51 0.49

test 0.51 0.49Processing final data for tensorflow format model

# match target

mTarget<-match("target",names(data))

# data processing for tensorflow

x_train <- data.matrix(train[,-mTarget])

x_test <- data.matrix(test[,-mTarget])

y_train <- as.numeric(FactorToBin(train$target,target))-1

y_train <- to_categorical(y_train, 2)

y_test <- as.numeric(FactorToBin(test$target,target))-1

y_test <- to_categorical(y_test, 2)Model

Set up sequential neural network model using Keras API. The sequential model makes the assumption that the network has exactly one input and exactly one output, and that it consists of a linear stack of layers.

- layer_dense: This layer can be interpreted as a function, which takes as input a 2D tensor and returns another 2D tensor—a new representation for the input tensor. Specifically, the function is as follows (where W is a 2D tensor and b is a vector, both attributes of the layer) output = relu(dot(W, input) + b) with dot product: between the input tensor and a tensor named W, vector b and relu: relu(x) is max(x, 0)

- activation function: Without an activation function like relu (also called a non-linearity), the dense layer would consist of two linear operations—a dot product and an addition: output = dot(W, input) + b So the layer could only learn linear transformations (affine transformations) of the input data: the hypothesis space of the layer would be the set of all possible linear transformations of the input data into a 16-dimensional space. Such a hypothesis space is too restricted and wouldn’t benefit from multiple layers of representations, because a deep stack of linear layers would still implement a linear operation: adding more layers wouldn’t extend the hypothesis space. In order to get access to a much richer hypothesis space that would benefit from deep representations, you need a non-linearity, or activation function. relu is the most popular activation function in deep learning, but there are many other candidates, which all come with similarly strange names: prelu, elu, and so on.

- input_shape: dimensionality of the input (integer) not including the samples axis. This argument is required when using this layer as the first layer in a model.

- layer_dropout: consists in randomly setting a fraction rate of input units to 0 at each update during training time, which helps prevent overfitting.

# dimension dataset

d<-dim(train)[2]-1

# set up model

model <- keras_model_sequential()

model %>%

layer_dense(units = 5, activation = 'relu', input_shape = d) %>%

layer_dropout(rate = 0.1) %>%

layer_dense(units = 7, activation = 'relu', input_shape = d) %>%

layer_dropout(rate = 0.1) %>%

layer_dense(units = 7, activation = 'relu', input_shape = d) %>%

layer_dropout(rate = 0.1) %>%

layer_dense(units = 2, activation = 'softmax')- Compile: to make the network ready for training, we need to pick three more things, as part of the compilation step:

- Loss function: how the network will be able to measure its performance on the training data, and thus how it will be able to steer itself in the right direction.

- Optimizer: the mechanism through which the network will update itself based on the data it sees and its loss function.

- Metrics: to monitor during training and testing.

# compile model

model %>% compile(

loss = 'categorical_crossentropy',

optimizer = optimizer_rmsprop(),

metrics = 'accuracy'

)

print(model)

Model

______________________________________________________________________

Layer (type) Output Shape Param #

======================================================================

dense_1 (Dense) (None, 5) 250

______________________________________________________________________

dropout_1 (Dropout) (None, 5) 0

______________________________________________________________________

dense_2 (Dense) (None, 7) 42

______________________________________________________________________

dropout_2 (Dropout) (None, 7) 0

______________________________________________________________________

dense_3 (Dense) (None, 7) 56

______________________________________________________________________

dropout_3 (Dropout) (None, 7) 0

______________________________________________________________________

dense_4 (Dense) (None, 2) 16

======================================================================

Total params: 364

Trainable params: 364

Non-trainable params: 0

______________________________________________________________________- Train your model

- epoch: number of iteration over all samples in the x_train and y_train tensors

- batch_size: mini batches

- validation_split: set of validation

# fit model

history <- model %>% fit(

x_train, y_train,

epochs = 20, batch_size = 100,

validation_split = 0.2

)

print(history)

Trained on 110,964 samples, validated on 27,742 samples (batch_size=100, epochs=20)

Final epoch (plot to see history):

val_loss: 0.5481

val_acc: 0.7107

loss: 0.559

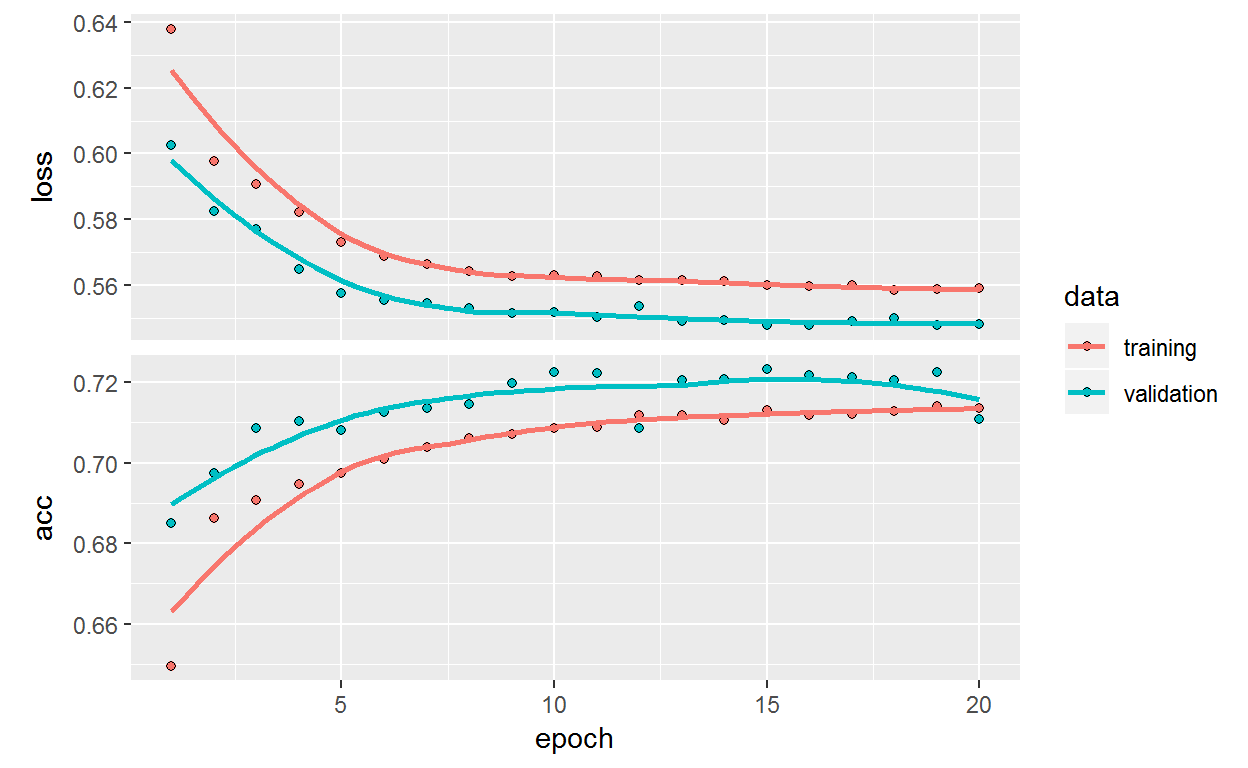

acc: 0.7135 Result of training

plot(history)

Model indicators

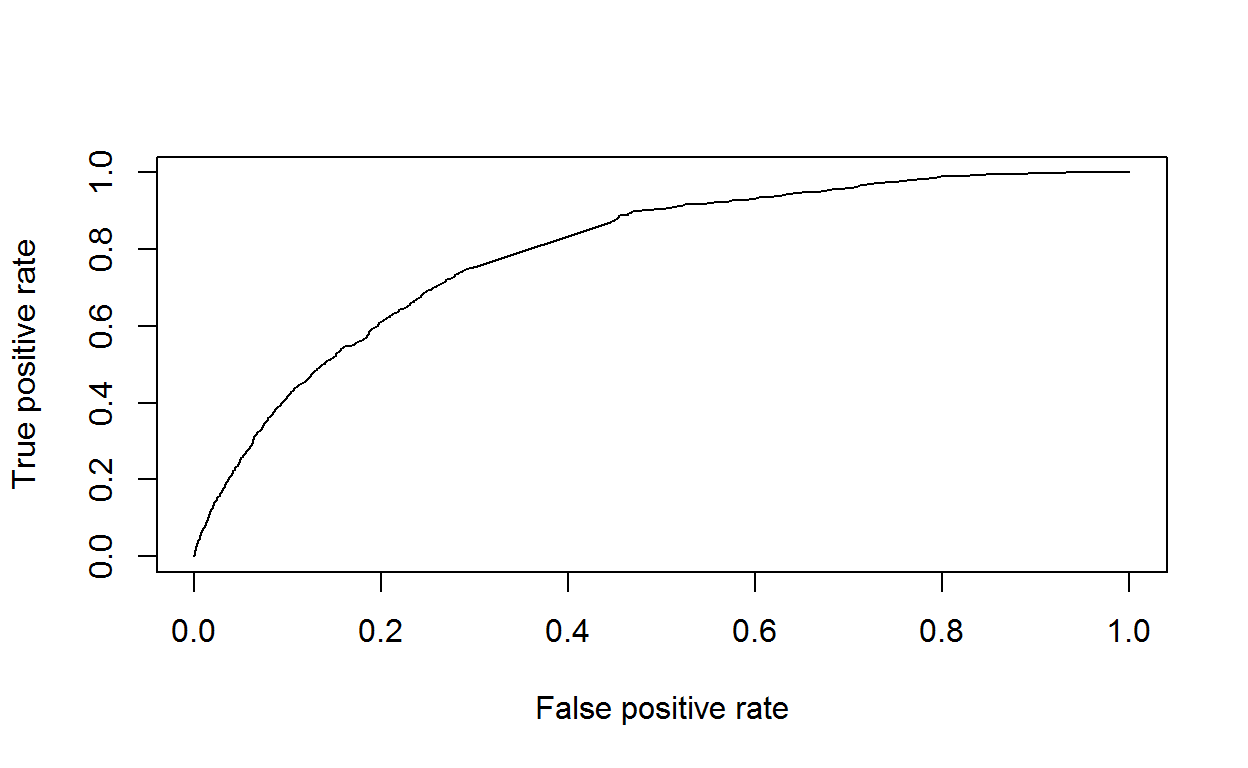

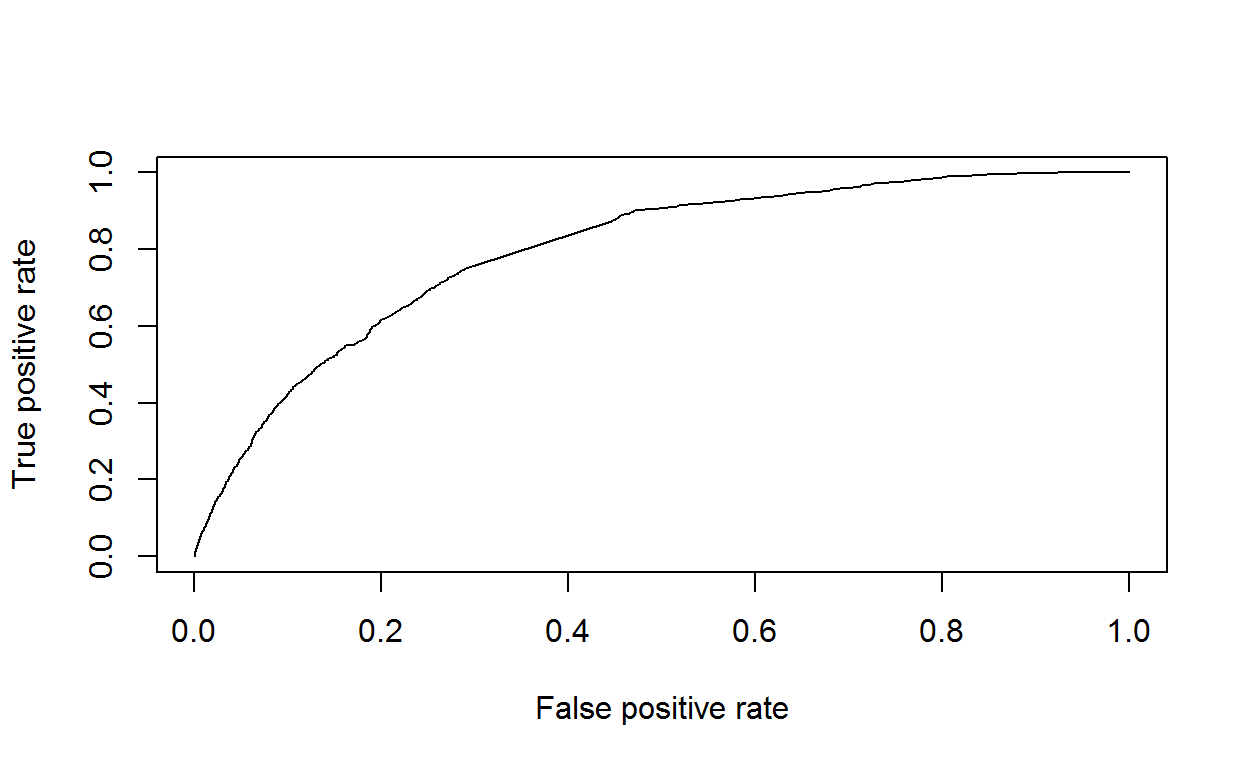

AUC is common metric on credit risk: AUC is area under the curve, In a ROC curve the true positive rate (Sensitivity) is plotted in function of the false positive rate (100-Specificity) for different cut-off points of a parameter. We’ll compute gini index: gini = 2*AUC-1.

model %>% evaluate(x_test, y_test)

$loss

[1] 0.5422537

$acc

[1] 0.7153551

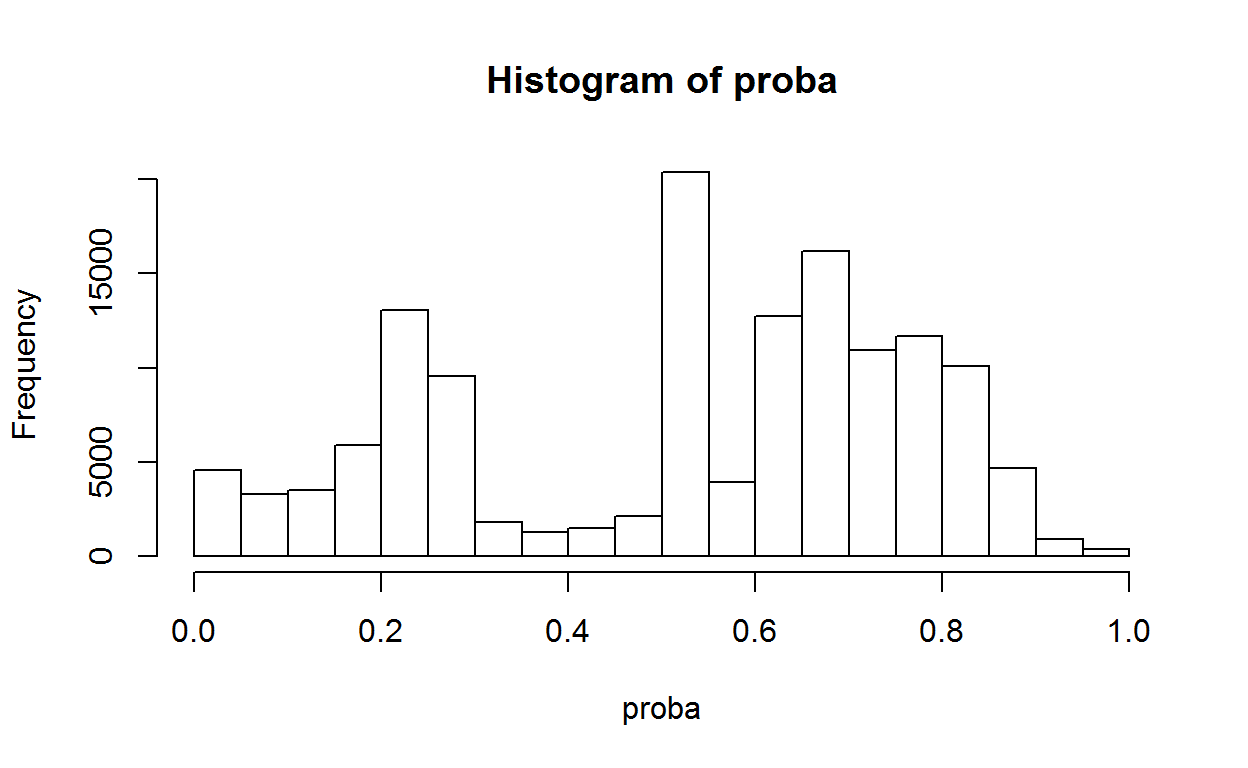

proba<-model %>% predict_proba(x_train)

proba<-proba[,2]

hist(proba)

ResTrain<-IndicatorsModels(train,proba,target)["gini"]

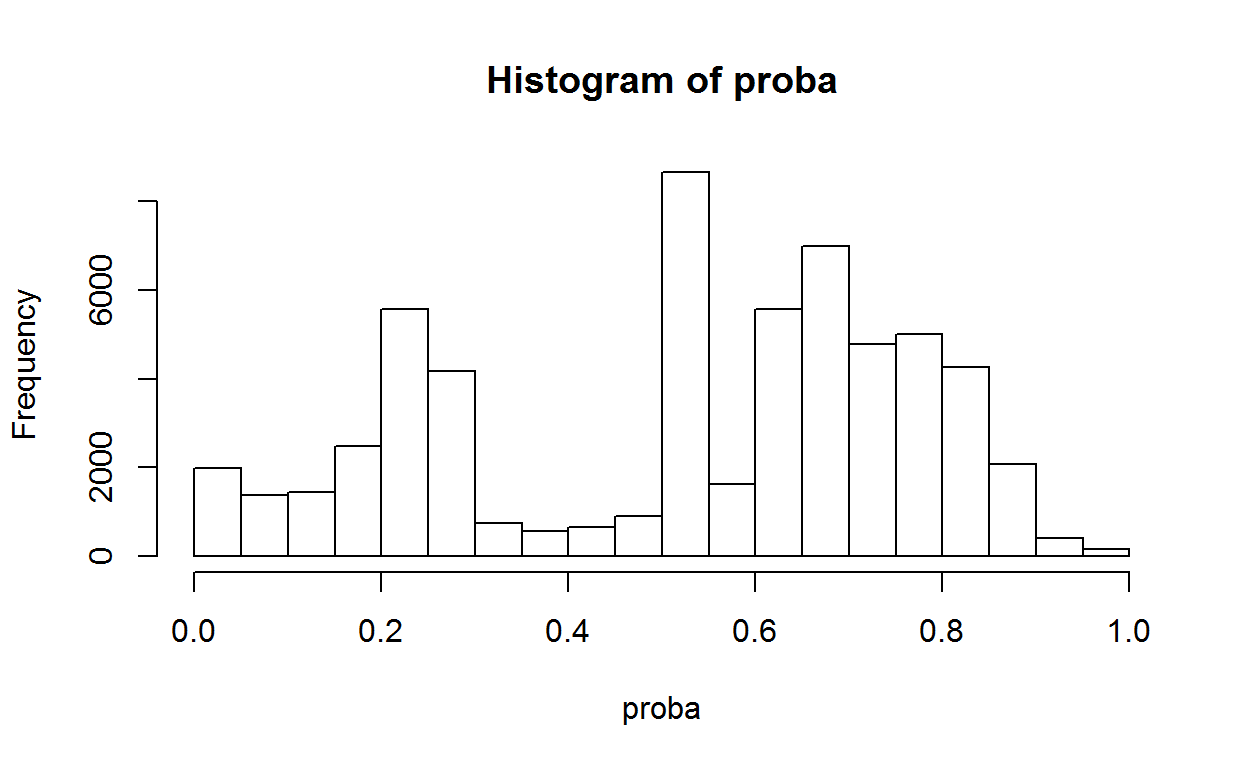

proba<-model %>% predict_proba(x_test)

proba<-proba[,2]

hist(proba)

ResTest<-IndicatorsModels(test,proba,target)["gini"]

res<-rbind(ResTrain,ResTest)

rownames(res)<-c("train","test")

print(res)

gini

train 59

test 59The gini index for train set is very close to test set, it’s a good thing. But the value of the index is bigger than 50%, it’s good result. Our model have a good predictive ability.

This example show how to use Keras API for binary classification and to measure the model performance with AUC.